")

Director’s View

Written by Johan de Villiers

Welcome to our latest quarterly newsletter. In this edition, I’ve been exploring a corner of the global technology economy that the international press has been shouting about, and the South African press, oddly, whispering about: the question of where the world’s artificial intelligence infrastructure is actually going to be built. You may have seen the headlines about $650 billion of hyperscaler capital expenditure this year, or about American data centre projects being cancelled at record rates. It turns out, the two stories are actually one story — and the strategic implications for South Africa are far more interesting than most people have noticed.

Industries Follow the Watts

The principle that compute-intensive industries migrate to wherever power is cheap and reliable is not a new one. The industrial revolution settled around the coalfields of northern England and the Ruhr Valley because steam power was geographically anchored. In the twentieth century, aluminium smelters — among the most electricity-hungry industrial operations on earth — were built almost without exception next to hydroelectric dams: Kitimat in British Columbia, Reykjavik in Iceland, Maputo in Mozambique. The product travelled to market; the smelter never moved from the dam.

When the early internet went looking for somewhere to put its first generation of hyperscale data centres, it gravitated toward the same logic. Cheap, stable power. Cool ambient temperatures. Abundant water for cooling. Sweden, Iceland and the Pacific Northwest of the United States picked up the bulk of that early build for exactly these reasons. More recently, when Bitcoin mining was forced out of China in 2021, it followed the watts again — this time to Texas natural gas, Kazakh coal and Icelandic geothermal.

What’s different now is the scale of the shift, and the speed at which it has arrived.

Enter the Hyperscalers

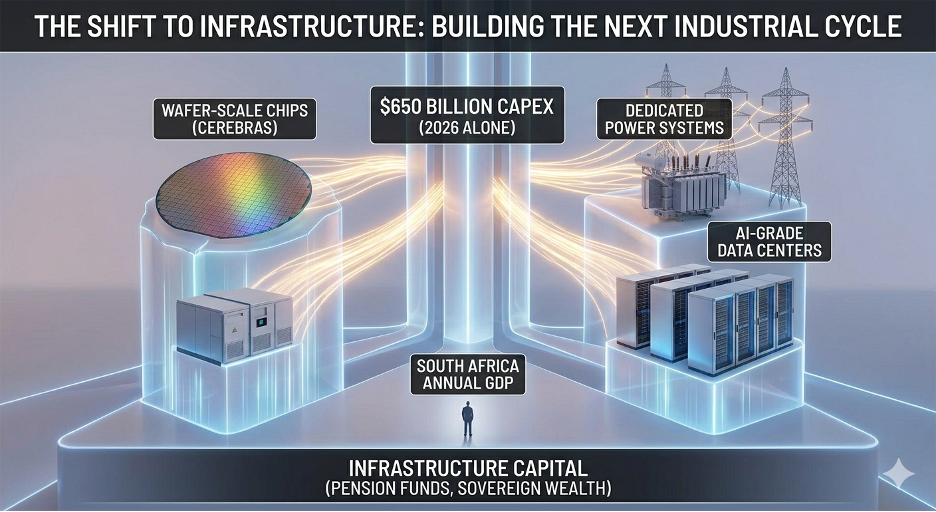

The four companies that dominate the AI infrastructure buildout — Alphabet, Amazon, Meta and Microsoft — are spending more than $650 billion on data centres, chips and the power systems to run them in 2026 alone. To put that figure in perspective, it is roughly twice the entire annual GDP of South Africa, deployed in a single year by four corporate balance sheets. The scale of the capital deployment is without recent precedent.

What is driving it is the realisation that the next decade of value creation in technology will run through infrastructure rather than through consumer applications. The market has voted decisively. KKR closed a more than $10 billion fund in early May 2026 to launch Helix Digital Infrastructure, a vehicle whose entire purpose is to design, build, own and operate AI-grade data centres alongside their own dedicated power generation. Cerebras priced its initial public offering at a $3.5 billion valuation in the same week, validating its wafer-scale chip thesis as a credible challenger to Nvidia. CoreWeave’s listing the year before had already opened that door; Cerebras simply walked through it.

The investors backing these moves are not technologists chasing the next consumer fad. They are infrastructure capital providers — pension funds, sovereign wealth, large institutional allocators — buying what they expect to be the picks-and-shovels layer of the next industrial cycle.

How It Actually Works

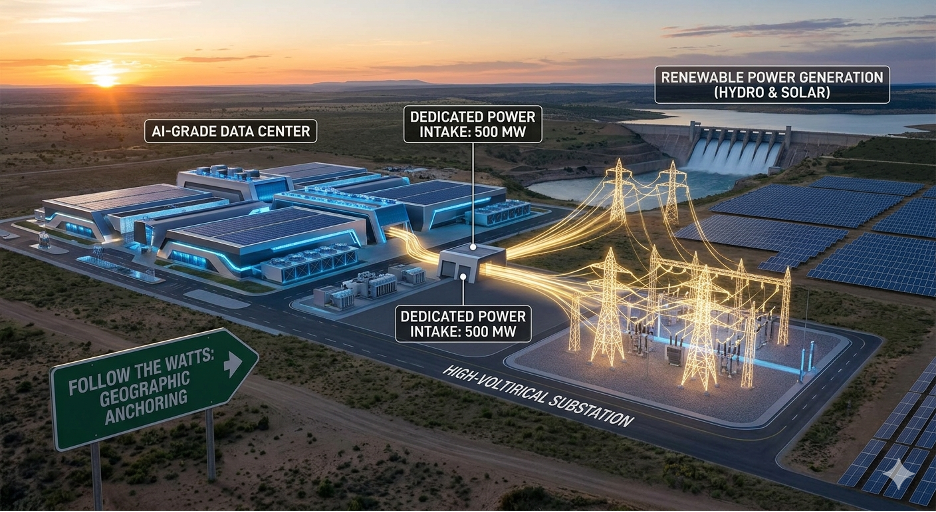

The mechanics of the new infrastructure are straightforward, if unfamiliar to anyone who hasn’t been watching this market closely. A modern AI data centre is a hyper-dense electrical load, drawing anywhere between 50 and 500 megawatts in continuous demand for a single facility. Five hundred megawatts is roughly the output of a mid-sized power station. It is also roughly the demand of a city of 400,000 people. Between 30% and 50% of all US data centres planned for 2026 — about 16 gigawatts of intended capacity — are now delayed or cancelled outright, primarily because the local grid cannot supply them. transformer lead times for new high-voltage substations have stretched to five years.

The result is that data centre operators have stopped waiting for utilities to catch up. The leading operators are now negotiating direct power purchase agreements with renewable generators, or in some cases commissioning their own dedicated generation. A facility’s economics now depend less on its proximity to fibre infrastructure — fibre is everywhere now — and far more on its proximity to surplus power.

This has produced a structural shift in where new data centre capacity is being built. Local opposition to large-scale data centre developments is mounting in North America and Europe, driven by concerns about water consumption, noise, and the visible strain on residential power supply. The infrastructure is being pushed outward, geographically, toward jurisdictions that have power, regulatory clarity, and political tolerance for the build.

The Promise and the Peril

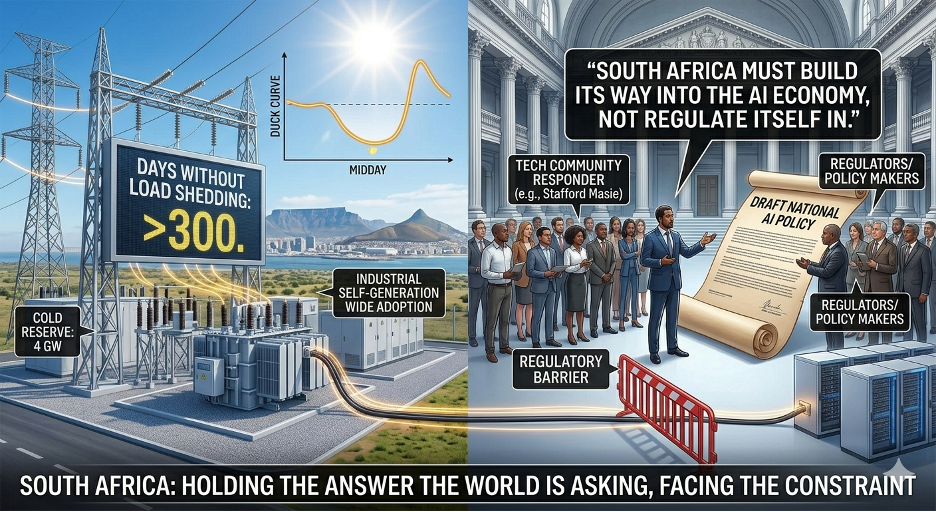

Which brings us to South Africa. As of April 2026, the country has gone more than 300 consecutive days without load shedding — load shedding being the local term for the scheduled rolling blackouts that defined our economic life for the better part of a decade. Eskom entered the year with 4.4 gigawatts of additional generation capacity. Peak national demand in March came in at approximately 26.5 gigawatts against available capacity that regularly exceeded 28 gigawatts, with nearly 4 gigawatts held in cold reserve because there was no demand to absorb it.

This is an inversion of the problem we have been engineering around for ten years. Rooftop solar has reshaped the residential demand curve so significantly that the duck curve — the midday collapse in grid demand driven by distributed generation — is now a measurable daily reality in the Western Cape and Gauteng. Industrial consumers have moved decisively to self-generation.

Data centre operators have already started moving. Teraco has built a 120-megawatt solar facility in the Free State and is wheeling that power to its sites in Cape Town and Johannesburg. Vantage Data Centers has secured 87 megawatts for its Waterfall City campus. The infrastructure supercycle that the rest of the world has run out of grid for is, quietly, beginning to land here.

The peril is regulatory. The Draft South African National Artificial Intelligence Policy, that was recently retracted, and the technology community’s response — articulated most forcefully by Stafford Masie in his open letter to Minister Solly Malatsi — is that the draft prioritises governance frameworks over the binding constraints of compute, capital, talent retention and energy access. Masie’s line cuts to the issue: “South Africa will not regulate its way into the AI economy. It must build its way into it.”

What It Means for the Rest of Us

Whether South Africa converts this moment into a structural advantage or merely watches it pass remains an open question. The truth, as is often the case, will probably sit somewhere in the middle. At the optimistic end, the country has every ingredient required to capture a meaningful share of the displaced global AI infrastructure build: surplus generation, a maturing renewables sector, our strategic time-zone position between Asia and the Americas, and intercontinental subsea cable connectivity that has improved markedly over the past three years. Twelve to eighteen months is a generous estimate of how long that window stays open before global supply catches up and the comparative advantage erodes.

At the cautious end, the country has a long track record of allowing policy debates and regulatory caution to outrun the underlying business case, and there is little obvious in the current draft AI policy to suggest that pattern is about to break.

What is undeniable is that the constraint has shifted. For two decades, the binding question for global technology investment was where to find compute, capital and talent. From 2026 onwards, the binding question is where to find power. South Africa has, almost by accident, ended up holding the answer to a question the world is only now learning how to ask.

Watch this space, because the substations, quite literally, are being built.

Warm Regards,

Johan de Villiers

CEO

First Technology Western Cape